All Categories

Featured

Table of Contents

That generally makes them a more economical option for life insurance policy protection. Numerous people obtain life insurance protection to help financially shield their loved ones in situation of their unforeseen fatality.

Or you might have the option to transform your existing term protection right into an irreversible policy that lasts the rest of your life. Numerous life insurance coverage plans have prospective advantages and drawbacks, so it's crucial to recognize each prior to you decide to purchase a plan.

As long as you pay the premium, your recipients will certainly get the fatality benefit if you die while covered. That stated, it is very important to note that most plans are contestable for two years which means insurance coverage could be rescinded on fatality, must a misstatement be discovered in the application. Plans that are not contestable often have a graded death advantage.

Costs are normally reduced than whole life plans. With a level term policy, you can choose your protection quantity and the policy length. You're not secured right into an agreement for the remainder of your life. Throughout your plan, you never need to stress over the costs or fatality benefit quantities transforming.

And you can not pay out your policy throughout its term, so you will not obtain any type of financial gain from your previous insurance coverage. As with various other sorts of life insurance policy, the cost of a degree term policy depends on your age, coverage needs, employment, way of life and health. Commonly, you'll discover extra inexpensive insurance coverage if you're younger, healthier and much less risky to guarantee.

Tax-Free Guaranteed Issue Term Life Insurance

Since degree term costs remain the same for the period of insurance coverage, you'll know specifically just how much you'll pay each time. Level term protection also has some adaptability, enabling you to personalize your policy with added functions.

You may have to meet certain problems and qualifications for your insurance firm to pass this cyclist. Additionally, there might be a waiting period of up to six months before taking effect. There also can be an age or time frame on the insurance coverage. You can include a kid biker to your life insurance policy so it likewise covers your children.

The death advantage is usually smaller, and coverage usually lasts up until your child transforms 18 or 25. This biker might be a more affordable way to assist guarantee your kids are covered as cyclists can typically cover numerous dependents simultaneously. Once your child ages out of this insurance coverage, it may be feasible to convert the cyclist right into a brand-new plan.

The most common kind of permanent life insurance policy is entire life insurance, however it has some key distinctions contrasted to level term coverage. Here's a fundamental introduction of what to take into consideration when contrasting term vs.

A Renewable Term Life Insurance Policy Can Be Renewed

Whole life insurance lasts insurance coverage life, while term coverage lasts insurance coverage a specific periodCertain The premiums for term life insurance coverage are typically lower than entire life protection.

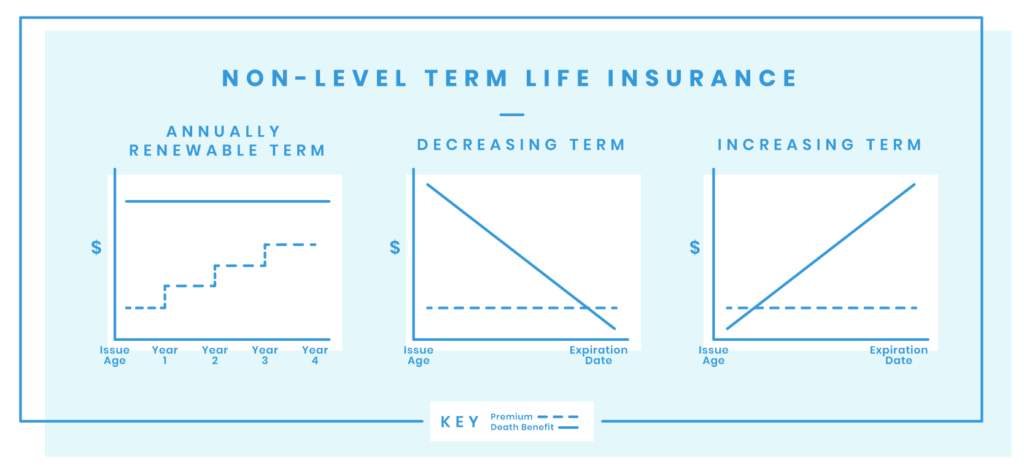

One of the highlights of level term insurance coverage is that your costs and your survivor benefit do not alter. With lowering term life insurance policy, your premiums continue to be the same; nonetheless, the survivor benefit quantity gets smaller in time. You may have protection that starts with a fatality advantage of $10,000, which could cover a home mortgage, and after that each year, the fatality advantage will reduce by a set amount or percentage.

Due to this, it's frequently an extra budget friendly type of degree term protection., however it may not be adequate life insurance policy for your demands.

After determining on a policy, complete the application. If you're approved, authorize the paperwork and pay your initial costs.

Quality Decreasing Term Life Insurance

Lastly, take into consideration scheduling time annually to assess your policy. You might wish to upgrade your beneficiary information if you've had any type of considerable life adjustments, such as a marriage, birth or separation. Life insurance policy can sometimes feel complicated. Yet you do not have to go it alone. As you discover your options, think about reviewing your needs, wants and worries about a monetary expert.

No, degree term life insurance policy doesn't have cash value. Some life insurance policy plans have a financial investment feature that allows you to build cash money value gradually. A part of your costs payments is set apart and can earn rate of interest over time, which expands tax-deferred throughout the life of your protection.

You have some choices if you still desire some life insurance policy coverage. You can: If you're 65 and your insurance coverage has run out, for example, you might want to get a new 10-year level term life insurance coverage plan.

Group Term Life Insurance Tax

You might have the ability to convert your term coverage into an entire life plan that will certainly last for the rest of your life. Many kinds of degree term policies are convertible. That implies, at the end of your protection, you can transform some or every one of your policy to entire life insurance coverage.

Level term life insurance is a plan that lasts a set term normally between 10 and three decades and includes a level survivor benefit and level costs that stay the same for the entire time the policy holds. This suggests you'll recognize precisely just how much your payments are and when you'll need to make them, permitting you to budget as necessary.

Level term can be a wonderful option if you're wanting to purchase life insurance policy coverage for the very first time. According to LIMRA's 2023 Insurance policy Measure Research, 30% of all grownups in the U.S. need life insurance policy and don't have any type of sort of plan yet. Degree term life is foreseeable and budget friendly, that makes it one of one of the most popular sorts of life insurance policy.

{kind=link}

Latest Posts

Final Expense Protect Commercial

Mutual Of Omaha Burial Policy

Best Funeral Plans For Over 50s