All Categories

Featured

Table of Contents

There is no payout if the policy expires prior to your death or you live beyond the policy term. You might be able to restore a term policy at expiration, yet the costs will be recalculated based on your age at the time of renewal.

At age 50, the costs would certainly climb to $67 a month. Term Life Insurance Policy Rates three decades old $18 $15 40 years of ages $28 $23 50 years old $67 $51 Source: Quotacy. Quotes are for a $250,000 30-year term life policy, for males and women in excellent wellness. In comparison, right here's a take a look at prices for a $100,000 entire life plan (which is a sort of long-term plan, implying it lasts your life time and includes cash money value).

Rate of interest rates, the financials of the insurance company, and state policies can also influence costs. When you take into consideration the quantity of coverage you can get for your costs dollars, term life insurance policy has a tendency to be the least expensive life insurance.

Thirty-year-old George wants to safeguard his family members in the not likely event of his early fatality. He gets a 10-year, $500,000 term life insurance coverage plan with a costs of $50 monthly. If George dies within the 10-year term, the policy will certainly pay George's recipient $500,000. If he dies after the plan has actually expired, his recipient will get no benefit.

If George is identified with a terminal health problem during the very first policy term, he probably will not be qualified to restore the plan when it ends. Some policies provide guaranteed re-insurability (without proof of insurability), however such functions come with a higher cost. There are several sorts of term life insurance.

Generally, a lot of companies supply terms varying from 10 to 30 years, although a couple of deal 35- and 40-year terms. Level-premium insurance coverage has a set month-to-month repayment for the life of the policy. A lot of term life insurance policy has a degree premium, and it's the kind we have actually been referring to in many of this write-up.

Premium What Is Direct Term Life Insurance

Term life insurance coverage is attractive to young individuals with children. Parents can obtain significant protection for a reduced expense, and if the insured passes away while the plan holds, the family members can rely upon the survivor benefit to replace lost earnings. These plans are likewise well-suited for individuals with expanding family members.

The best option for you will certainly rely on your requirements. Below are some things to take into consideration. Term life policies are perfect for individuals that want considerable coverage at an inexpensive. Individuals that possess entire life insurance policy pay much more in costs for much less insurance coverage yet have the safety of knowing they are secured for life.

The conversion biker ought to enable you to convert to any type of long-term plan the insurance provider supplies without limitations. The primary features of the motorcyclist are preserving the original wellness score of the term plan upon conversion (also if you later have wellness concerns or become uninsurable) and determining when and how much of the insurance coverage to transform.

Of training course, total premiums will certainly boost dramatically considering that whole life insurance policy is extra costly than term life insurance policy. The advantage is the assured authorization without a medical examination. Clinical conditions that create throughout the term life period can not trigger costs to be raised. The company may require minimal or full underwriting if you desire to include additional cyclists to the brand-new plan, such as a long-term treatment motorcyclist.

Term life insurance policy is a fairly inexpensive method to offer a round figure to your dependents if something happens to you. It can be an excellent choice if you are young and healthy and balanced and sustain a family members. Whole life insurance policy features considerably higher regular monthly costs. It is indicated to supply coverage for as lengthy as you live.

Sought-After A Whole Life Policy Option Where Extended Term Insurance Is Selected Is Called

It depends on their age. Insurance coverage firms established an optimum age limitation for term life insurance coverage plans. This is normally 80 to 90 years old yet might be higher or reduced relying on the business. The costs likewise increases with age, so a person aged 60 or 70 will certainly pay significantly greater than a person decades more youthful.

Term life is rather comparable to auto insurance policy. It's statistically unlikely that you'll require it, and the premiums are cash down the tubes if you do not. If the worst occurs, your household will obtain the benefits.

The most prominent kind is now 20-year term. A lot of companies will not sell term insurance to a candidate for a term that ends previous his or her 80th birthday. If a policy is "sustainable," that suggests it proceeds active for an extra term or terms, approximately a specified age, even if the wellness of the guaranteed (or other elements) would certainly cause him or her to be rejected if he or she requested a new life insurance policy plan.

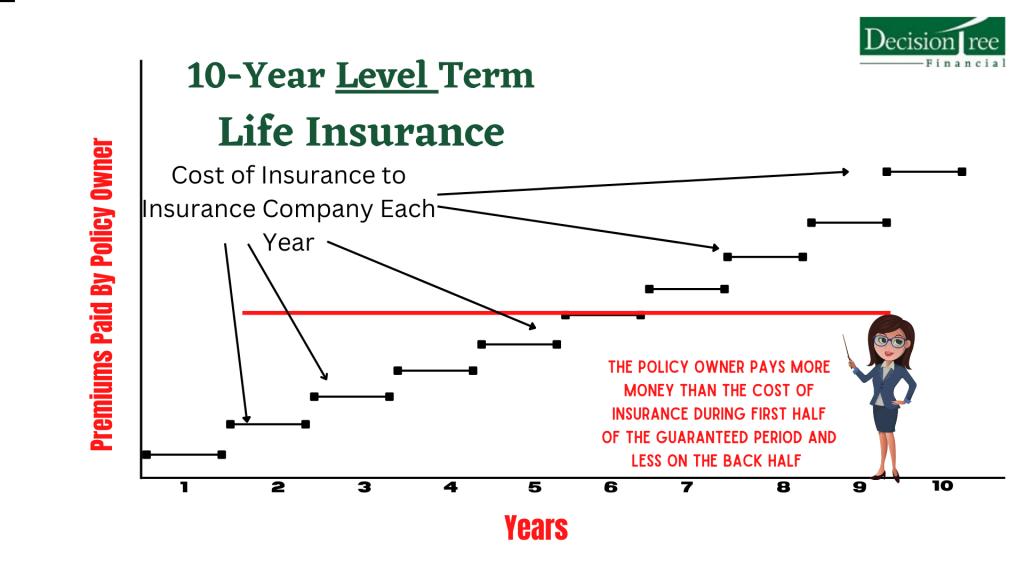

Premiums for 5-year eco-friendly term can be degree for 5 years, after that to a new price showing the new age of the insured, and so on every 5 years. Some longer term plans will assure that the costs will certainly not enhance during the term; others do not make that assurance, allowing the insurance coverage firm to raise the price during the policy's term.

This suggests that the policy's proprietor can change it into a long-term type of life insurance without added proof of insurability. In most types of term insurance policy, including homeowners and automobile insurance, if you haven't had a case under the plan by the time it expires, you get no refund of the costs.

Family Protection Guaranteed Issue Term Life Insurance

Some term life insurance policy customers have been dissatisfied at this outcome, so some insurance firms have actually created term life with a "return of premium" function. term 100 life insurance. The costs for the insurance coverage with this attribute are frequently substantially higher than for policies without it, and they usually need that you keep the plan effective to its term or else you waive the return of costs benefit

Level term life insurance policy premiums and survivor benefit stay constant throughout the plan term. Level term plans can last for periods such as 10, 15, 20 or three decades. Degree term life insurance policy is generally much more budget friendly as it doesn't construct money worth. Level term life insurance policy is among the most common kinds of security.

Preferred Increasing Term Life Insurance

While the names often are utilized reciprocally, degree term coverage has some crucial differences: the premium and survivor benefit remain the very same for the duration of protection. Level term is a life insurance policy plan where the life insurance coverage premium and survivor benefit stay the exact same throughout of insurance coverage.

{kind=link}

Latest Posts

Final Expense Protect Commercial

Mutual Of Omaha Burial Policy

Best Funeral Plans For Over 50s